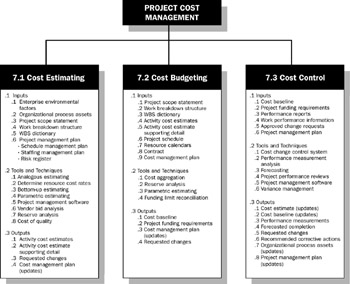

Project Cost Management includes the processes involved in planning, estimating, budgeting, and controlling costs so that the project can be completed within the approved budget. Figure 7-1 provides an overview of the following three processes, while Figure 7-2 provides a process flow view of these processes and their inputs, outputs, and other related Knowledge Area processes:

7.1 Cost Estimating – developing an approximation of the costs of the resources needed to complete project activities.

7.2 Cost Budgeting – aggregating the estimated costs of individual activities or work packages to establish a cost baseline.

7.3 Cost Control – influencing the factors that create cost variances and controlling changes to the project budget.

These processes interact with each other and with processes in the other Knowledge Areas as well. Each process can involve effort from one or more persons or groups of persons based upon the needs of the project. Each process occurs at least once in every project and occurs in one or more project phases, if the project is divided into phases. Although the processes are presented here as discrete elements with well-defined interfaces, in practice they may overlap and interact in ways not detailed here. Process interactions are discussed in detail in Chapter 3.

Project Cost Management is primarily concerned with the cost of the resources needed to complete schedule activities. However, Project Cost Management should also consider the effect of project decisions on the cost of using, maintaining, and supporting the product, service, or result of the project. For example, limiting the number of design reviews can reduce the cost of the project at the expense of an increase in the customer’s operating costs. This broader view of Project Cost Management is often called life-cycle costing. Life-cycle costing, together with value engineering techniques, can improve decision-making and is used to reduce cost and execution time and to improve the quality and performance of the project deliverable.

In many application areas, predicting and analyzing the prospective financial performance of the project’s product is done outside the project. In others, such as a capital facilities project, Project Cost Management can include this work. When such predictions and analyses are included, Project Cost Management will address additional processes and numerous general management techniques such as return on investment, discounted cash flow, and investment payback analysis.

Project Cost Management considers the information requirements of the project stakeholders. Different stakeholders will measure project costs in different ways and at different times. For example, the cost of an acquired item can be measured when the acquisition decision is made or committed, the order is placed, the item is delivered, and the actual cost is incurred or recorded for project accounting purposes.

On some projects, especially ones of smaller scope, cost estimating and cost budgeting are so tightly linked that they are viewed as a single process that can be performed by a single person over a relatively short period of time. These processes are presented here as distinct processes because the tools and techniques for each are different. The ability to influence cost is greatest at the early stages of the project, and this is why early scope definition is critical (Section 5.2).

Although not shown here as a discrete process, the work involved in performing the three processes of Project Cost Management is preceded by a planning effort by the project management team. This planning effort is part of the Develop Project Management Plan process (Section 4.3), which produces a cost management plan that sets out the format and establishes the criteria for planning, structuring, estimating, budgeting, and controlling project costs. The cost management processes and their associated tools and techniques vary by application area, are usually selected during the project life cycle (Section 2.1) definition, and are documented in the cost management plan.

For example, the cost management plan can establish:

Precision level. Schedule activity cost estimates will adhere to a rounding of the data to a prescribed precision (e.g., $100, $1,000), based on the scope of the activities and magnitude of the project, and may include an amount for contingencies.

Units of measure. Each unit used in measurements is defined, such as staff hours, staff days, week, lump sum, etc., for each of the resources.

Organizational procedures links. The WBS component used for the project cost accounting is called a control account (CA). Each control account is assigned a code or account number that is linked directly to the performing organization’s accounting system. If cost estimates for planning packages are included in the control account, then the method for budgeting planning packages is included.

Control thresholds. Variance thresholds for costs or other indicators (e.g., person-days, volume of product) at designated time points over the duration of the project can be defined to indicate the agreed amount of variation allowed.

Earned value rules. Three examples are: 1) Earned value management computation formulas for determining the estimate to complete are defined,

2) Earned value credit criteria (e.g., 0-100, 0-50-100, etc.) are established, and 3) Define the WBS level at which earned value technique analysis will be performed.

Reporting formats. The formats for the various cost reports are defined.

Process descriptions. Descriptions of each of the three cost management processes are documented.

All of the above, as well as other information, are included in the cost management plan, either as text within the body of the plan or as appendices. The cost management plan is contained in, or is a subsidiary plan of, the project management plan (Section 4.3) and may be formal or informal, highly detailed or broadly framed, based upon the needs of the project.

The cost management planning effort occurs early in project planning and sets the framework for each of the cost management processes, so that performance of the processes will be efficient and coordinated.

| Note |

Note: Not all process interactions and data flow among the processes are shown. |